Author: Kyle

Compiled by: Luffy, Foresight News

The biggest problem in the cryptocurrency field is not the shortage of talents or the lack of funds, but simply the lack of thinking based on first principles. This culture needs to be changed, and the top 1% group needs to lead the field forward.

If you follow my Twitter, you will find that I have been strongly advocating focusing on those seemingly easy-to-reach opportunities with high leverage, which seem extremely simple, but apparently no one can really "understand" or execute well.

In this article, I will specifically discuss some topics, including:

Compound interest assets, industry culture, short-termism

The universal Layer 1 blockchain is dead, and it is urgent to change

The relationship between liquidity tokens and investment

Buyback and destruction is just the least bad choice, not the best solution

I named this article "First Principles" because when I use common sense to think and imagine how to change this industry in the current situation, I came up with all these views.

In fact, the principles are not that profound. The definition of insanity is to do the same thing over and over again and expect different results. In three market cycles, we have been doing the same thing over and over again: basically creating illusory, value-accumulating, and highly exploitative tokens and applications, because for some stupid reason, we believe that every four years, this "casino" will open in a frenetic way, attracting funds from all over the world to participate in gambling.

Guess what? After three market cycles, that is, ten years, people finally woke up and realized that the casino's house, cheaters, fraudsters, manipulators, and those who sell you high-priced food and drinks in the casino are taking all your money. After months of effort, the only thing you can show is the on-chain record of how you lost everything. An industry where everyone wants to "come in, make money, and leave" cannot nurture any long-term compound interest assets.

This field used to have a good look, it used to be a place for real financial innovation and cool technology. We used to be excited about novel and interesting applications, new technologies, and "changing the future of finance".

But due to some extreme short-termism, highly exploitative culture, and dishonest people, we have fallen into this cycle of persistent financial nihilism, which is to some extent collectively caused by everyone thinking that buying the tokens issued by scammers who shout "buy the dip" is a good idea, because "I will withdraw before the scam collapses".

You can say that I don't have entrepreneurial experience, and that's true. This field is not large in scale and not long in existence. I have worked in this field for four years and collaborated with some of the best and brightest funds, which has given me an understanding of what works and what doesn't.

I reiterate: insanity is to do the same thing over and over again and expect different results. As an industry, we go through the same thing year after year: when the price inevitably crashes, we all feel that nihilism, feeling that everything is worthless. I felt this way when the NFT market collapsed; now, after the recent Memecoin chaos, people also feel this way; in the ICO era, people felt the same way.

The solution is actually very simple: we just need to start doing different things.

1. Compound interest assets, industry culture, short-termism

Compound interest assets simply means assets that appreciate in value over time, such as Amazon, Coca-Cola, Google, etc. Companies that own compound interest assets have the potential to achieve sustainable long-term growth.

Why haven't we seen compound interest assets in the crypto field?

The answer is a bit complex, but the root cause is extreme short-termism and misaligned incentives. Kun raised a very good point here:

"This is also why most things get reasonably valued or even overvalued after growing a few times, because they are traded based on the valuation of growth tech stocks in traditional finance, but they are just getting started, and most startups fail to go public. But here (in the crypto field), every failed project can still issue tokens just on the basis of a promise."

https://x.com/0x_Kun/status/1898599628448387482

Indeed, there are many problems with the way incentive mechanisms are constructed, and Cobie's article articulates this well. I won't go into depth, as the focus of this article is, what can we as individuals do now?

For investors, the answer is obvious. As Cobie pointed out in the article: you can choose to exit (and you probably should).

Indeed, people have chosen to exit. In this cycle, we have seen the decline of "centralized exchange (CEX) tokens" as retail investors no longer buy these tokens. While individuals may not have the ability to change this systemic problem, the good news is that financial markets are quite efficient: people want to make money, and when the existing mechanisms cannot achieve this, they will not invest, and the whole process becomes unprofitable, forcing the mechanisms to change.

However, this is only the first step of the process. To truly build compound interest assets, companies need to start instilling long-term thinking in this field. The problem is not just that "private market capture" is bad, but the entire chain of thinking that has led us to this point is problematic. Like a self-fulfilling prophecy, founders seem to collectively believe "I need to make money and then leave", with no one truly interested in long-term building, which means the charts always present a McDonald's "M" pattern.

The most critical point that must change is: the goodness of a company depends on its leadership. The reason most projects fail is not the lack of developers, but the decision of the top management to leave. This industry must start to see those founders with high integrity, strong execution, and long-term thinking as role models of effort, rather than idolizing those who "pump and dump".

The average quality of crypto founders is not high, which is no news. After all, calling people who hype up shitcoins "developers" doesn't set the bar very high. As long as you have a long-term vision in the first two months after the token launch, you're already ahead of the rest.

I also believe the market will start to economically incentivize long-termism, and we are already seeing this trend. Despite the recent selloff, Hyperliquid's price is still 4 times the initial issue price, which is a feat that few projects in this cycle can boast about. When you know the founder's long-term growth goals are aligned with the product, it's easier to convince yourself to "hold this project long-term".

The natural conclusion drawn from this is that founders with high integrity and strong execution will start to occupy the largest market share, because frankly, when everyone is tired of scams, they just want to work for someone with a vision who won't exit fraudulently, and such people are really too few.

In addition to having an excellent leader, building compound interest assets also depends on whether the product itself is excellent. In my view, this problem is easier to solve than finding an outstanding founder. One reason there are so many "shitcoin" projects in the crypto field is that the people who create these "shitcoins" also have the same "make money and leave" mentality, so they choose not to solve brand new problems, but to copy popular projects in an attempt to make money.

Here is the English translation of the text, with the specified terms translated as instructed:However, this industry does indeed reward such illusory ideas, such as the artificial intelligence agent hype in Q4 2024. In such cases, once the hype subsides, we will see the common McDonald's "M" shaped trend. Therefore, companies must also start focusing on developing profitable products.

No profitability path = No long-term believers / holders = No asset buyers, as there is no future to bet on

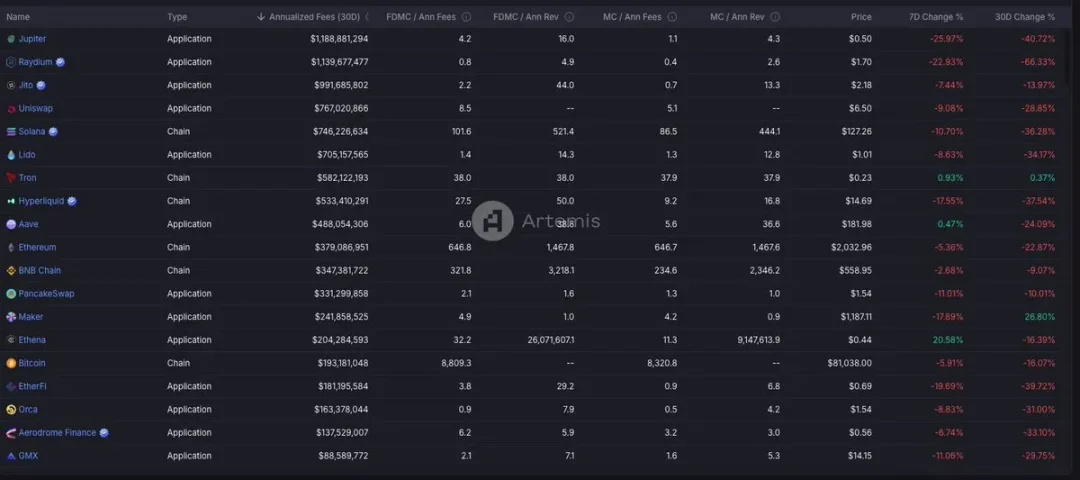

This is not an impossible task, as crypto companies can indeed be profitable. Jito has an annual revenue of $900 million, Uniswap $700 million, Hyperliquid $500 million, and Aave $488 million, and they continue to be profitable even in a bear market (just not as much).

Looking ahead, I believe that the fleeting, narrative-driven speculative bubbles will become smaller and smaller. We have already seen this trend. In 2021, the valuations of gaming and Non-Fungible Tokens (NFTs) reached hundreds of billions of dollars, but in this cycle, the valuations of Memecoins and artificial intelligence agents have only reached tens of billions of dollars at most.

I believe everyone is free to invest in whatever projects they want. But I also believe that people want their investments to generate returns. When the game becomes so obvious, becoming a "hot potato that I must get rid of before it goes to zero," the roller coaster will get faster and faster, and the market size will get smaller and smaller as people choose to exit or lose all their money.

Profitability can solve this problem. As an investor, it allows you to understand that people are willing to pay for this product, thereby achieving long-term growth to a certain extent. When a project has no profitability path, it is almost uninfestable in the long run. On the other hand, a profitability path will bring a growth path, which will attract buyers who are willing to bet on the continued growth of the asset.

In summary, building compounding assets requires:

Leaders with long-term thinking

Focus on developing profitable products

2. The Universal L1 is Dead, Transformation is Urgently Needed

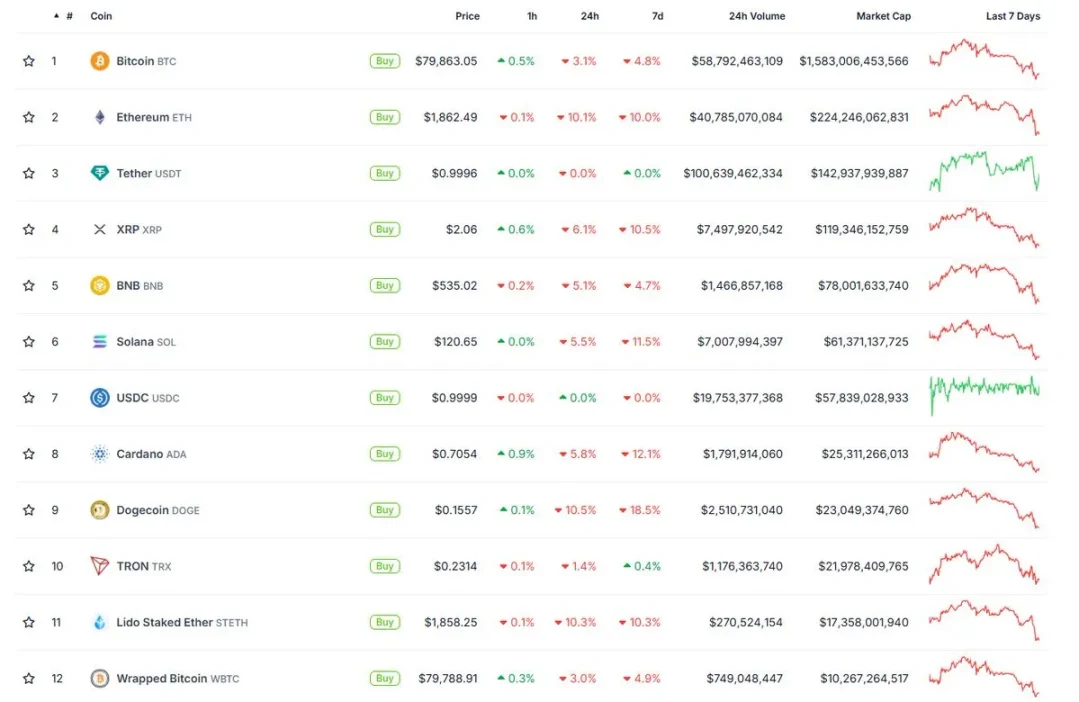

If you sort the CoinGecko website's homepage by market capitalization, you'll find that L1 blockchain projects account for more than half of the share. Apart from stablecoins, L1 occupies a large portion of the value in the crypto industry.

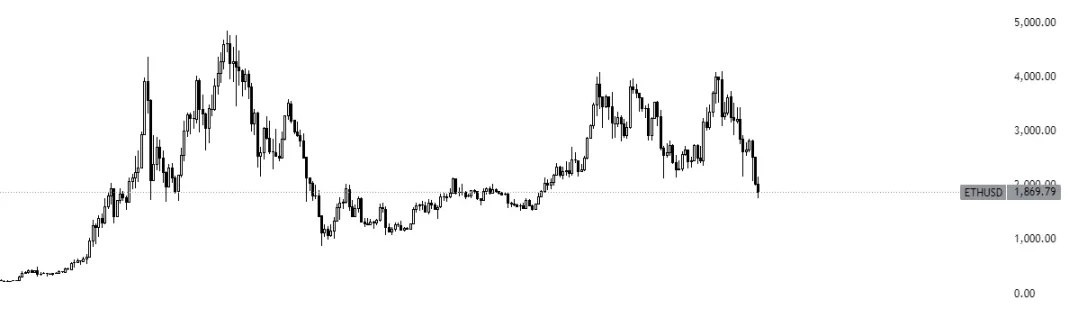

However, the price chart of Ethereum, the second-largest cryptocurrency after Bitcoin, looks like this:

If you bought Bitcoin in July 2023, your current gains would be 163%.

If you bought Ethereum in July 2023, your current gains would be 0%.

This is not the worst case. The "everything bubble" of 2021 sparked a wave of "Ethereum killers." Some new L1 blockchain projects tried to outperform Ethereum in certain technical aspects, mainly focusing on speed, developer languages, block space, etc. But despite the constant hype and massive investment, the results have not met expectations.

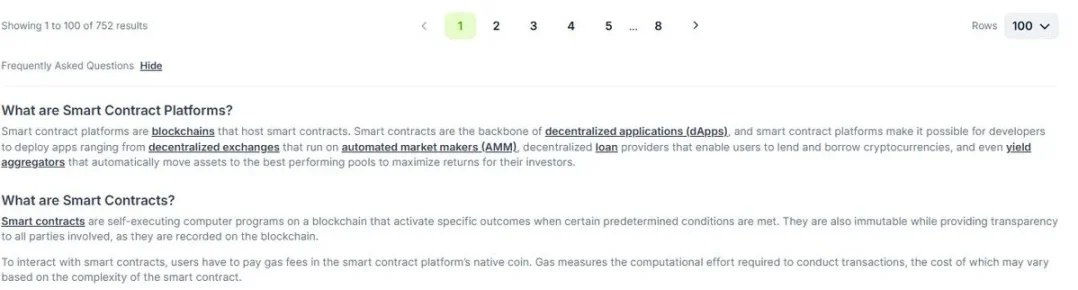

Now, 4 years after 2021, we are still feeling the impact of that wave. On CoinGecko, there are already 752 smart contract platforms that have issued tokens, and there may be even more that have not issued tokens.

Unsurprisingly, the price charts of most of them look like this, while Ethereum's chart looks relatively better:

So, despite 4 years of effort and billions of dollars invested, with over 700 different blockchain projects, only a few L1s have decent activity, and even those haven't achieved the "breakthrough user adoption" that was expected 4 years ago.

Why? Because the design philosophy of most of these projects is flawed. As Luca Netz pointed out in his article "What is Consumer Crypto," many blockchains today are adopting a universal model, with each project dreaming of being able to "host the internet economy."

But this requires massive effort and ultimately leads to market fragmentation, as a product that tries to do everything usually ends up doing nothing well. It's a task that consumes a lot of money and time. Frankly, many blockchains can't even answer a simple question: "Why should we develop on your blockchain instead of the 60th blockchain?"

The state of L1 is another example of everyone following the same pattern but expecting different results. They compete for the same limited developer resources, trying to outdo each other in funding programs, hackathons, developer studios, and now it seems we're developing phones (?).

Suppose an L1 project succeeds. In each cycle, there will be some L1 projects that can break through. But will that success be sustainable? The success story of this cycle is Solana. But here's a view that many may not like: What if Solana becomes the next Ethereum?

In the last cycle, many were so convinced that Ethereum would succeed that they invested most of their net worth in it. Ethereum still has the highest Total Value Locked (TVL), and there are even Ethereum ETFs now, yet its price has stagnated. In this cycle, the same people are making the same claims, believing that Solana is the future of blockchain, and even anticipating a Solana ETF and so on.

If history can be a reference, the real question is: Can today's success guarantee tomorrow's relevance?

Rethinking L1

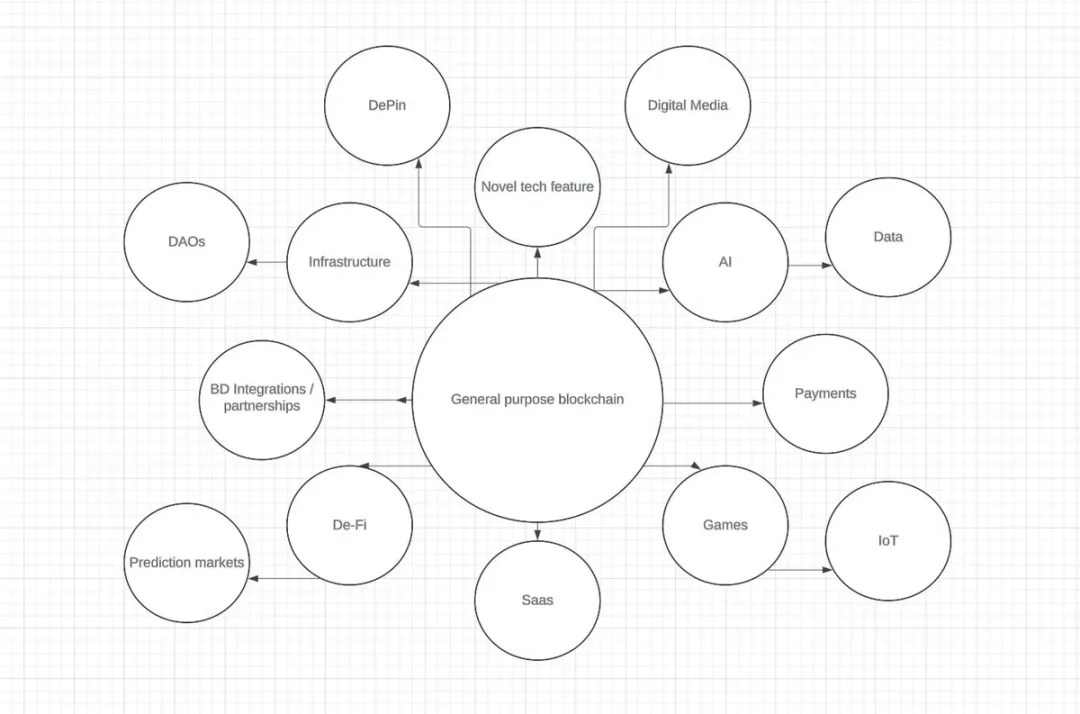

My view is simple: Rather than building universal blockchains, it would be wiser for L1s to be built around a core focus. A blockchain doesn't need to meet everyone's needs; it just needs to serve a specific purpose. I believe the future of blockchain will be independent of the underlying blockchain, and people will only care about its performance, while the technical details won't be as important.

Developers have already shown signs of this: For founders of decentralized applications, the main concern is no longer how fast the blockchain runs, but the user distribution and end-user usage of the blockchain. Does your blockchain have users? Does it have the user distribution needed to make the product appealing?

44% of web traffic comes from WordPress, yet its parent company Automattic is only valued at $7.5 billion. 4% of web traffic comes from Shopify, but its valuation is $120 billion, 16 times that of Automattic! I think L1s will have a similar end state, where their value will accrue to the applications built on the blockchain.

So, I think L1s should boldly build their own ecosystems. If we use cities as an analogy for blockchains, we can see that cities have risen due to their specific advantages, making them viable economic and social hubs, and over time, these cities have specialized in certain leading industries or functions:

Silicon Valley → Technology

New York → Finance

Las Vegas → Entertainment and Hospitality

Hong Kong and Singapore → Trade-focused financial centers

Shenzhen → China's hardware manufacturing and tech innovation hub

Paris → Fashion, art, and luxury

Seoul → K-pop, entertainment, and beauty industry