Author: Maxxx

A confession from a frontline crypto market maker, a self-help guide to the dark forest of project parties, hoping to be of some help to you:)

Let me introduce myself: I'm Max, a 00s who feels very old, originally a poor finance student from Hong Kong, but I've been in the crypto industry (thanks to the industry for saving me) since 2021. Although I haven't been in the industry for long, I entered the industry as a project party at first, and later started my own business doing a developer community and accelerator, so I've always been quite close to the frontline entrepreneurs. Now I'm in charge of our market making business line at @MetalphaPro, thanks to the boss for giving me the title of Head of Ecosystem, but it's actually just responsible for BD and sales. In the past year or so, I've been involved in the listing and subsequent market making of more than a dozen coins on @binance, @okx, @Bybit_Official and second-tier exchanges, so I have some shallow experience.

It's been a turbulent spring recently, and the topic of market makers has also been in the spotlight. I've always wanted to talk about the special role of market makers in the industry in a systematic way, and this is a good opportunity for me to do some sorting out. My business is not very sophisticated, and if there are any flaws, please forgive me. This article represents my own views and is 100% written by me.

Here's a photo of my dog to end this

Starting from the "observation tag" of GPS...

When I heard that GPS had been given an "observation tag" by @binance, I was chatting with the founder of a project that I had known for more than a year and was planning to list in Q2. This gentleman is very young, handsome, and capable, but you can hear the fatigue in his tone - the project has raised a few Mil, achieved some good results, and everything seems to be going well, but for the founder, the money raised is actually debt, constantly pivoting the narrative for over a year, the market is so difficult, trying to close a new round of financing on one hand, negotiating with top-tier exchanges on the other hand, and worrying about the recent token price performance, how to account to investors, the hardship, worries and confusion can only be understood by those who have done projects... Just as we were chatting, Binance's notice suddenly caught our eye, and although we didn't have any market making cooperation with the project, we had been in touch with the team members for the past two years, and we were suddenly full of emotion.

I won't analyze or comment too much on this matter, as that would be long-winded and unattractive. We'll just wait for Binance and the project party's notifications and announcements. But over the past two years, I've seen too many project parties and retail investors being scammed by market makers, and this is a good opportunity for me to write this article, hoping to help project parties and practitioners. Okay, enough chit-chat, let's get down to business.

The business model of market makers: not as magical as it's said, just a "quote maker"

Market making is not a new term in the crypto industry, as there are also "market makers" in the traditional financial industry, but this service has a more relaxed name, called Greenshoe (because in 1963, the Boston Greenshoe Company used this mechanism for the first time during its IPO). Although the mechanism is slightly different, the responsibilities are basically the same, which is to provide two-way quotes in the IPO to maintain market liquidity and relative price stability. However, due to strict compliance regulations, the Greenshoe business is a very standard trading desk business with little "oil and water", and not even a major trading desk will PR it as a separate business. But ironically, this standard business has become a "scythe" in the eyes of many people in the crypto industry, controlling the market.

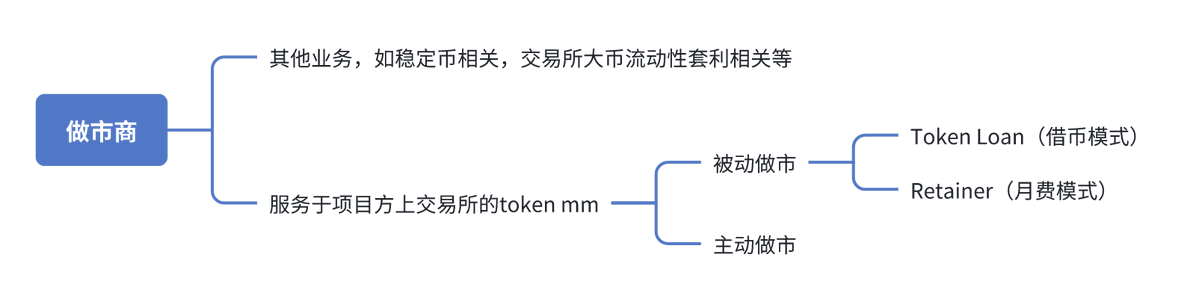

However, if market makers really follow industry standards and provide liquidity in a standardized manner, there is nothing like a "scythe". The so-called provision of liquidity is mainly to provide two-way quotes on the trading order book. Of course, the broader definition of crypto market makers also includes some other categories and businesses, but today we'll just focus on the narrow category that serves the token listing of project parties, which can be roughly divided into the following business models:

Active Market Makers

Much of the demonization of market makers in the industry actually stems from the existence and operations of active market makers in the early days of the industry. There's a Cantonese saying "doing the kitchen", which in Mandarin is called "doing the yard", and active market makers satisfy all the fantasies of the "market maker". Generally, active market makers will cooperate with project parties to directly manipulate the market price, inflate or suppress, and profit from it, harvesting the retail investors, and sharing the profits with the project parties. Their cooperation terms are also diverse, involving borrowing coins, accessing APIs, leveraging, profit sharing, etc. There are even rogue market makers who don't communicate with the project parties, but directly use their own capital to grab the tokens, and then operate the market themselves after accumulating enough tokens.

Who are the active market makers in the market? In fact, the market-active PR, event-holding, and well-known market makers are all passive market makers, at least they must claim to be, otherwise they will have compliance issues, let alone do marketing openly (but it's not ruled out that some market makers have done some active cases in the early days of the industry, or are still secretly doing so now).

Most active market makers are very low-key, and don't have a name, because they are non-compliant. As the industry becomes more standardized, the previously high-profile ZMQ and Gotbit have been named by the FBI and are in serious compliance trouble, and the remaining active market makers are also more incognito, some of the bigger ones have done some so-called "successful cases", so they have "local influence", and their main deals are through personal referrals.

Passive Market Makers

Passive market makers, including ourselves and many other peers, belong to this category, and their main job is to provide two-way maker quotes on the order book of centralized exchanges to provide market liquidity. The business model is mainly divided into two types:

Token Loan

Retainer

Token Loan

This is the current mainstream and most widely used cooperation model. In simple terms, it's a model where the tokens are lent to the market maker for a certain period of time, and the market maker provides market making services.

A typical token loan deal consists of several parts:

Loan amount x%: Generally a percentage of the token's total supply

Loan term x months: The duration of the loan, and the service will end upon maturity, with delivery according to the pre-signed option

Option structure: The delivery price for the market maker at the end of the service

Liquidity KPIs: The depth of the quotes the market maker will provide on the order book, possibly involving different exchanges and price ranges.

How do market makers make money in this model?

Market makers make money in two parts, one is the spread between the buy and sell quotes during the quoting process, which is generally a small part; the other is the options given to the market makers by the project parties, which is generally the main part.

Here is the English translation of the text, with the specified terms translated as requested:If you are familiar with finance, you may know that every option has value on the first day of signing, which is a percentage of the borrowed token value. For example, if I borrowed a total of 100,000 tokens, and the option's value on the first day is 3%, it means that if I strictly follow the algorithm (delta hedge) to place orders, I can realize a relatively certain profit of $30,000. In general (excluding extreme situations such as a skyrocketing or rapidly zeroing Bit price, which cannot be effectively delta hedged), the trading desk's profit from this collaboration is $30,000 plus some money earned from the bid-ask spread.

Does it feel like market makers are earning more than expected? But in fact, the profit margin I mentioned is not completely unrealistic, as market makers are also very competitive now, and the prices of competitive options are also becoming less liquid.

Retainer (monthly fee model)

This is currently the second relatively mainstream model, which means that the project party does not lend Tokens to the market maker, but retains them in their own trading account, and the market maker accesses the market through the API. The advantage of this model is that the Tokens are still in the hands of the project party, and all the operations in the trading account are transparent to the project party, so there is no need to worry about the risk of the market maker's misconduct. However, in this model, the project party needs to prepare Tokens and U in the account for two-way order placement, and generally needs to pay a monthly service fee to the market maker.

In this case, the market maker places orders according to the customer's liquidity KPI, and earns the monthly service fee. The funds in the account are not related to the market maker, and in the case of poor liquidity/needle insertion, the order placement will lose money, and these losses will be borne by the project party.

I think Token loan and Retainer both have their pros and cons, some exchanges will only focus on one, and some like us can do both. Project parties should choose based on their own needs and project situation.

Several common misconceptions

Market makers are responsible for "pumping the market", "drawing lines" and "building mouse nests"

Qualified passive market makers are neutral, and will not actively participate in pumping the market, market capitalization management, or harvesting.

Market makers providing liquidity is "wash trading"

The order book of the exchange has two types of orders, maker orders and taker orders. Passive market makers mainly place maker orders, and the proportion of taker orders will be very small. Without counterparty takers to execute the maker orders placed on the order book, it cannot directly increase the trading volume. However, if the market maker self-trades their own maker orders, i.e. "self-trading", there will be compliance risks, and top exchanges will also strictly scrutinize this behavior. If the self-trading ratio is too high, the market maker's account and Tokens may face warnings and actions from the exchange.

So it seems that passive market makers are not very useful?

Not directly responsible for Bit price or trading volume, it may seem that way. But good liquidity is the foundation of everything. Small-scale money cares more about Bit price trends, while large capital needs to look at trading volume and depth as the first thing to enter. A token with active trading and healthy Bit price is closely related to the product strength and marketing capabilities of the project party, and indeed requires close cooperation with market makers. Even a step back, top-tier exchanges will rarely let you list without a professional market maker, otherwise it will likely be a mess at launch, so market makers are a necessary step for every project party to list on top CEXs.

It sounds like market making is just order placement, and the threshold is not high, so the project party can do it themselves?

Yes and no. If you do have an in-house trading team and your project is relatively large, some second-tier exchanges may allow you to do it yourself. But if you don't, or need to build a new team, I still suggest letting professionals handle it. On the one hand, the cost and risk of building a team is not worth it compared to finding a reliable market maker. On the other hand, if you are not familiar with market making, you will actually lose a lot of money when facing various extreme market conditions.

The ecological position of market makers: opening liquidity is the most valuable resource

After popularizing the business models, let's talk about the current situation, which may help you understand better.

What will the crypto market be like in 2024-2025? From the perspective of liquidity, I see it this way:

BTC has an independent market, rising all the way up, top-tier liquidity is sufficient, there has been a recent correction, but the foundation is not shaken, miners' mining costs are starting with 5 or 6, they are very happy, and the traditional institutions rushing in are also happy

The tail-end PVP is fierce, and liquidity was once relatively sufficient, @pumpdotfun, @gmgnai, @solana, @base and @BNBCHAIN small investors are losing money with great enthusiasm (I also contributed a bit, damn it), outliers and insiders are also happy making money

Mid-tier liquidity is depleted, with the trump and libra wave as the peak, it has almost sucked out the liquidity and buy-side of the mid-tier, and it is structurally and irreversibly transferred from the inside to the outside, tokens with market caps from hundreds of millions to tens of billions are in an awkward position, newly listed tokens on top-tier exchanges have no buyers, the trading volume and depth mostly occur at launch, and they quickly fall below the VC's primary price, and after VC unlocking, they are likely to lose money, and after team token unlocking, they are likely to go to zero

In this cycle, these mid-tier tokens seem to be having the toughest time. But another cruel fact is that more than 90% of the so-called "web3 native" practitioners in our industry, who are the real ones getting paid, receiving salaries, attending conferences, and doing business, including VCs, project parties, accelerators, BD, marketing, developers, etc., are all doing business with these mid-tier tokens. You look at investment and financing, product development, market promotion, hair-pulling, and exchange listing, it is actually centered around these centralized exchange mid-tier project parties. So in this cycle, many practitioners have not made money, and their days have not been good either.

Only market makers, I think, hold the scarcest resource of mid-tier tokens: "opening liquidity". Yes, liquidity alone is not enough, it needs to come early, be there at launch, otherwise when the project goes to zero, having a lot of Tokens is useless. A project's opening circulating supply may be 15%, and 1-2 percentage points, or even more, are given to market makers. This opening, immediately unlocked liquidity is an extremely valuable resource in the current market. Therefore, not only are market makers becoming more and more competitive, but many VCs and project parties are also joining the temporary team to start doing MM, some teams even without basic trading capabilities, just take the Tokens first and worry about it later, since they will end up going to zero anyway.

The Dark Forest of Driving Out Good Coins with Bad Coins: Honest Paying Personalities Cannot Match "Scumbags"

Under this market evolution, a very unique ecology of market makers has formed today: on the one hand, there are more and more market makers, with quotes spiraling to an absurd degree; on the other hand, the quality of service and professional capabilities vary greatly, with various after-sales problems often occurring, the most common of which is withdrawing liquidity and defaulting on the market. First of all, it is clear that market makers are not prohibited from selling coins, in fact, if the coin price soars, according to the algorithm, the order should be biased towards the selling direction, because the coin I borrowed is the one I need to settle with the project party (those who don't understand can take another look at the token loan option part).

But a qualified passive market maker should place orders normally according to the algo, rather than being a taker and slamming the market, which is a huge damage to the project. Why do market makers do this? Going back to the option part we just talked about, a market maker who has obtained a token loan quota, if the market is lukewarm, he should successfully realize the value of the option and make 3%. But if he believes that the project will go to zero at the time of settlement, he can realize a 100% return by opening and slamming the market, which is 33 times the normal mm earnings. Of course, this is the most intuitive and extreme example, most real operations will be much more complicated, but the underlying logic is, to short the token, sell it when the price is high and liquidity is good, and then buy it back to settle at maturity.

Of course, in addition to being unethical and non-compliant, this also has additional risks. On the one hand, the market maker is completely unable to provide liquidity according to the KPI within the contract period, because he does not have a healthy inventory; on the other hand, if the token is bet in the wrong direction, he will lose a lot of money and be unable to pay.

Why is this behavior so common?

At the end of the day, the compliance of the industry is still in its early stages. In the case of the token loan model, although market makers will report the service situation to the project party through daily reports, weekly reports, dashboards, etc., and there are also third-party supervisory institutions and tools in the market, what the market makers do with the tokens in their accounts is still a black box, and the market lacks effective regulatory measures. After all, the only ones who have conclusive evidence and can see every trade of the market makers are the centralized exchanges themselves, but many of the market makers are V8 V9 clients of the centralized exchanges, bringing billions of dollars in commissions and deposits to the exchanges every year, and the exchanges also have an obligation to protect the privacy of their clients, so how could they possibly make public the trading details of the market makers to help the project parties with their rights protection? Speaking of this, I can't help but admire @heyibinance @cz_binance for their decisive action. As far as I know, this is the first time the trading details of market makers have been publicly disclosed, including the precise time down to the minute, the operational details and the cash-out amount. Whether this behavior should be done is worth pondering, but the original intention must be good.

The project parties, including the entire industry, still need to strengthen their understanding of market makers. In fact, what surprised me a lot is that I have talked to many top-tier investors, founders of projects that have raised tens of millions of dollars, and even practitioners in the exchanges, and they are not very familiar with this profession of market makers, which is also an important reason why I decided to write this article. Because most project parties are actually "first-timers", but the market makers are "scumbags" with rich experience. As a frontline practitioner, sometimes when I see the project parties choosing the so-called "better terms", I will also ask myself, should I also match the absurd terms offered by the competitors and get the deal done first? In this dark forest of market makers, it is difficult to hold the bottom line, and the pretentious scumbags are always more attractive than the honest and upright, only when everyone's understanding of the industry is aligned can we avoid the situation of bad coins driving out good coins from continuing to occur.

How to Choose Your Market Maker

There are a few questions and tips that I think are important:

Is it always wrong to choose an active market maker?

In fact, when project parties ask me this question, I won't directly say don't choose them. If we put aside compliance, I think this is a question worth debating. Some projects have indeed brought better charts, more trading volume, and more cash-outs through close cooperation with active market makers, although the number of those who have messed up is also countless. Here I just want to express one point of view, you need to be aware that those who can really help you pull in real money will also not hesitate to cut you, and at the end of the day, the market's liquidity is limited, you are opponents, the market's money either you earn or your active market maker earns.

Should you choose token loan or retainer for the cooperation?

Currently, the token loan model is still more mainstream, but the market share of retainer is slowly rising. This is a matter of the project party's taste and demand, for example, projects that want to maintain tight control may not want to have uncontrollable large liquidity from the outside, and so on.

Try not to choose only one passive market maker

Don't put all your eggs in one basket, you can choose 2-4 market makers, compare the terms with each other, and if one of them goes down, the others can fill in. In addition, market makers usually propose various additional value-adds in order to win the deal, choosing multiple parties can get more help from them. However, to avoid the problem of "three monks have no water to drink", it is recommended to assign different exchanges to the market makers, as the difficulty of monitoring will increase linearly if they are mixed together.

Don't just choose your market maker based on their investment

You can accept the investment from the market maker, and having more runway is always good. But you also need to understand that the investment of market makers is not playing the same game as VC investment, because they control a considerable part of the opening liquidity, market makers can easily lock the price and hedge the tokens they have invested in but not yet unlocked, so the tokens borrowed by market makers may not be 100% a good thing for the project party.

Don't just choose your market maker based on liquidity KPIs

Liquidity KPIs are very difficult to verify in practice, so don't just choose market makers based on liquidity KPIs, no matter how beautifully the terms are written, if they can't deliver, it's useless. Before lending the tokens, you are the father, but once the tokens are lent to the market makers, you become the son, and they have many ways to fool you.

Change your mindset: become a "scumbag" yourself

Remember that you are the client, before signing the mm, compare the terms more, talk more about how to monitor and prevent the market makers from defaulting, and choose the solution that suits your project development. You can use the terms of one party to pressure the other, go back and forth to compare the terms, and don't have any ambiguity in the terms, if there are any unclear points, don't try to figure it out yourself, just ask directly.

A Few Thoughts

I am a junior in the industry, and I am very grateful to have the opportunity to perceive and touch the industry in such depth. I often feel the dirtiness and chaos of the industry, but also the vitality and vitality at all times. I have never thought of myself as the smartest of the bunch, there are many excellent young people in the industry of the same age as me who have quickly found their own position, but more young people are actually very confused, if it weren't for the web3 industry, it would be difficult for them to find a channel for upward mobility.

I also have a highly principled boss and a professional trading team doing the back-end. The stable asset management business allows us not to rely on the market making business to support the team, but to use the market making business to make friends. I have also been following my own pace, with the logic of making friends with project parties, missed some deals, but also talked to a few deals that I am proud of, and some projects, although not successful in business, have also become friends with the project parties.

I have rambled on a lot, and the process of releasing this article has been very conflicted for me, on the one hand I am afraid that my business is not proficient enough, or that my expression is not good enough, and I have misled the project parties and readers, on the other hand, market makers have always been taboo in the industry, and I am also afraid that I will not grasp the scale properly and touch someone's cake.

But I really think that as the industry develops, compliance gradually becomes mainstream, and one day, the role of market makers will no longer be demonized, but will return to the sunshine, and I hope this article can play a small part in this.