Valuation Controversy in the Market Frenzy: The "Low FDV" Trap of BGB and Concerns over Financial Reserves

Bitget CEO Gracy Chen recently emphasized the "low fully diluted valuation (FDV)" of BGB - the current price of $5.03 corresponds to an FDV of only $6 billion, far lower than the $96 billion of BNB and the $25.9 billion of HT. However, this narrative has two core flaws: the valuation of exchange tokens is based on trading volume and ecosystem support, while Bitget's actual financial reserves and market share are far from sufficient to support its FDV rationality.

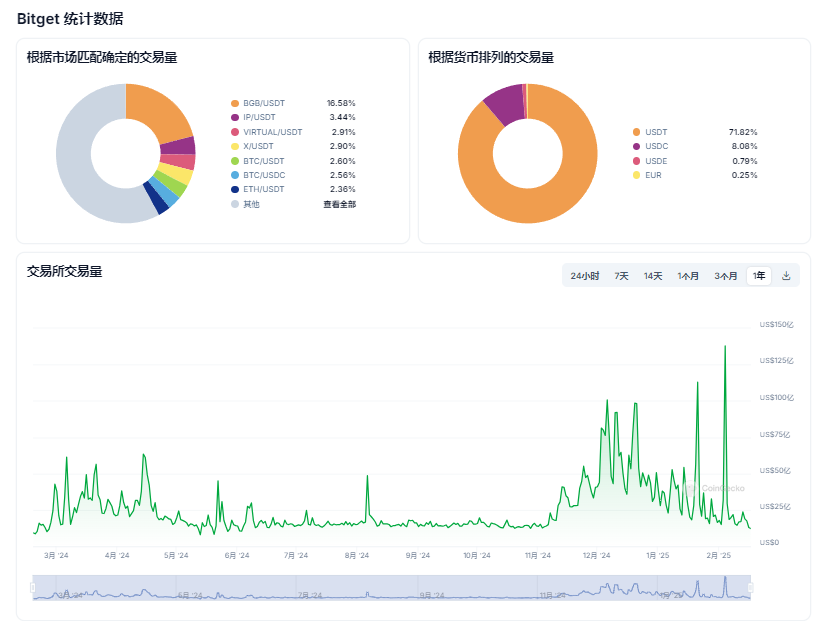

First, from the perspective of financial reserves, Bitget's published Merkle tree asset proof shows that its overall reserve ratio is as high as 217% (BTC reserve ratio 499%, USDT 134%), but the total asset size is only about $4 billion, and USDT reserves account for an extremely small proportion. In contrast, Binance's USDT reserve size is as high as $27 billion, and its spot and derivatives trading volume accounts for more than 45% of the global market share, while Bitget's trading volume accounts for less than 10%. This means that Bitget's "high reserve ratio" is essentially due to a small asset base, while Binance has formed stronger risk resistance and value support with its huge capital pool and trading volume.

Secondly, the FDV/trading volume ratio further exposes the valuation bubble. If calculated based on Bitget's official daily trading volume of $20 billion (annualized about $7.3 trillion), its FDV/trading volume ratio is 0.008 ($6 billion/$7.3 trillion), higher than Binance's 0.005 ($96 billion/$180 trillion). This is contrary to its market share - the market capitalization and trading volume contribution are seriously out of balance, which is essentially a speculative valuation logic of "betting big with small".

More worryingly, the circulation design of BGB has flaws. Although Bitget announced the destruction of 40% (800 million) of the total supply by the end of 2024, its subsequent quarterly buybacks depend on 20% of the platform's profits. However, Bitget has not disclosed specific profit data, and its revenue is highly dependent on the highly volatile derivatives trading (accounting for more than 80%). If the market declines, the buyback strength may shrink, and the actual effect of the destruction mechanism is doubtful.

Conclusion: The "low FDV" of BGB is essentially an illusion of valuation created by small-scale assets and trading volume, lacking sustainable financial and ecological support. The gap between its financial reserves and market share compared to Binance further reveals the fragility of its valuation logic.

The "Paper Prosperity" of Ecological Expansion: User Growth ≠ Value Capture

Another major selling point of Bitget is its ecological expansion - integrating the BWB wallet token, layout of the PayFi payment scenario, and expansion of DeFi and NFT businesses. However, these initiatives are more at the strategic level and have not yet formed a substantial moat.

Taking the merger of BWB and BGB as an example, although this move aims to unify the ecological tokens, the merged BGB has not significantly improved the application scenarios. Although Bitget Wallet claims to have 60 million users, its main functions are still limited to asset storage and cross-chain exchange, lacking differentiated competitiveness compared to mature wallets like MetaMask.

More critically, the core demand for BGB is still limited to platform-internal privileges (such as fee discounts and Launchpool participation rights), lacking external application scenarios. This is in stark contrast to BNB, which has penetrated the blockchain gaming, DEX, lending protocols and other full-chain ecosystems, and even become a compliant currency for offline payments in some countries. The "internal circulation" attribute of BGB makes its value highly dependent on Bitget's own development, and once the platform growth slows down, the token will face selling pressure.

Lack of Market Makers and Doubts about Price Manipulation

Regarding the community's questioning of the "lack of independent market makers", Bitget has never responded directly. According to on-chain data analysis, the main liquidity of BGB is concentrated in Bitget's own wallet addresses, and there have been large-scale transfers and abnormal price fluctuations multiple times in the past six months. For example, in October 2024, BGB plummeted 42% in a single day, and Bitget calmed the controversy by "compensating user losses with the protection fund", but did not publicly disclose the specific trading records.

This "both referee and player" model has raised market concerns about price manipulation. In contrast, top exchanges like Binance and OKX have introduced multiple third-party market makers and disclosed their market-making strategies through transparency reports. Bitget's closed-door operations not only undermine investor trust, but may also exacerbate price volatility risks due to insufficient liquidity.

Survival Crisis in the Industry Turmoil: CEX Red Ocean Competition and Regulatory Sword

The cryptocurrency exchange arena in 2025 has entered a cruel elimination period. On the one hand, giants like Binance and Coinbase are consolidating their advantages through compliance and global expansion; on the other hand, emerging DEXs (such as Uniswap and dYdX) are grabbing market share with lower costs and higher transparency. Bitget's middle position - neither a fully compliant CEX nor a pure on-chain protocol - is facing double squeeze.

Although CEO Gracy Chen emphasized that "Bitget has no plans to sell", the industry M&A wave is heating up. In 2024, cases such as Kraken's acquisition of Gemini and Bybit's integration of FTX's remaining business indicate that the independent survival space of mid-sized CEXs is increasingly narrow. If Bitget fails to break through in compliance licenses and technological innovation, it may be difficult to escape the fate of being integrated.

Regulatory risks cannot be ignored either. The US SEC has recently strengthened its scrutiny of CEXs, requiring the disclosure of token economic models and conflict of interest information. If Bitget fails to prove the non-security nature of BGB, it may face the risk of delisting or litigation - this hidden danger has not yet been fully priced by the market.

Reverse Deduction: The Potential Collapse Path of BGB - Three Major Catalysts for a Decline from $5 to $3

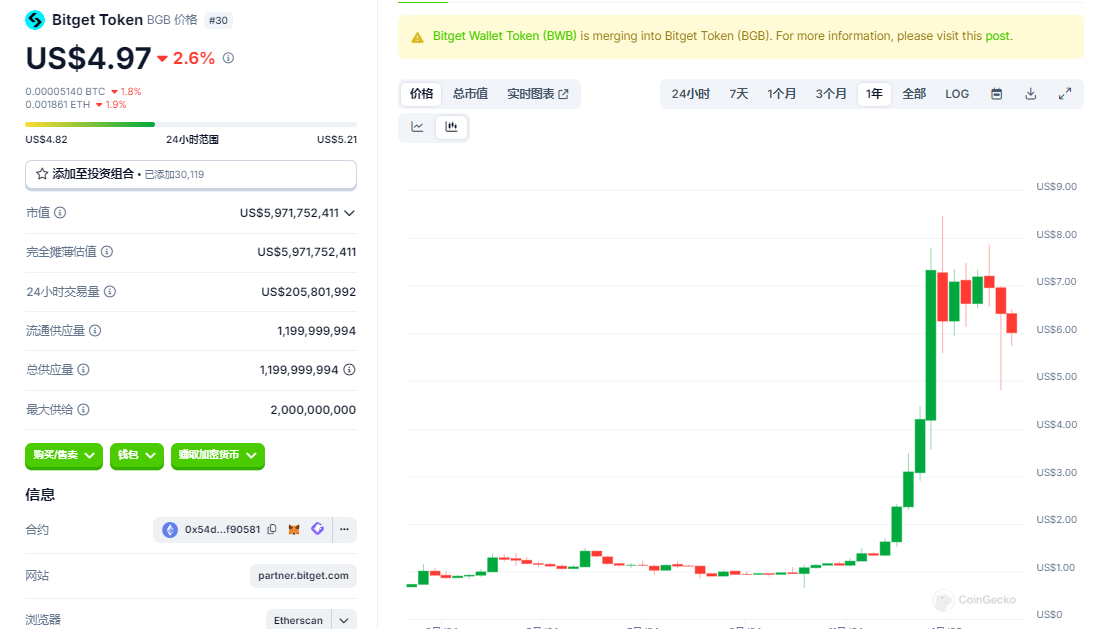

Supporters view BGB's recent drop from $8.5 to $5 (a 42% decline) as a "healthy correction", similar to the 44% correction in mid-2024. However, the backgrounds of the two corrections are completely different: the previous decline occurred in the overall bear market of cryptocurrency altcoins, while the current market is in a bull cycle with BTC reaching a new high. BGB's counter-trend plunge is more likely to reflect its intrinsic value being overpriced.

From a technical perspective, BGB's weekly RSI and MACD are showing divergence signals, and trading volume has been shrinking, indicating that the main capital is withdrawing. The so-called "destruction benefit" has already been priced in - after the announcement of the destruction in December 2024, BGB briefly surged to $8.5 and then quickly fell back, forming a typical "good news exhausted" pattern.

Even based on the bullish calculation model, the valuation logic of BGB still has fatal flaws. If the V/MC ratio, trading volume growth rate, and deflationary mechanism are subjected to reverse pressure testing, it can be found that its price has the risk of halving to $3.

1. Deterioration of V/MC ratio: Liquidity trap and market capitalization collapse

According to the valuation logic of cryptocurrency exchange tokens, the V/MC ratio (trading volume/market capitalization) is an important indicator to measure their liquidity and market acceptance. Referring to the practices of industry leaders and market analysis, the healthy V/MC ratio of exchange tokens should be controlled below 10%, reflecting a reasonable level of trading activity and market value matching.

Benchmark reference for top exchanges

Taking Binance (BNB) as an example, its spot and derivatives daily trading volume in 2024 was about $1 billion, corresponding to a market capitalization of $96 billion, with a V/MC ratio of about 0.5% ($1 billion/$96 billion≈1%). This ratio reflects the effective support of high trading volume for market value, and is within the "healthy range" recognized by the market.

Valuation risks of mid-sized exchanges

If the V/MC ratio of the exchange token is significantly higher than 1% (such as 3%-5%), it may imply two major risks:

- Doubts about the authenticity of trading volume: Some platforms may artificially inflate data through wash trading or high-frequency trading, leading to an inflated V/MC ratio.

- Market capitalization bubble: Low market capitalization combined with high trading volume can easily form a short-term speculative premium, but lack long-term ecological support.

The current V/MC ratio (trading volume/market capitalization) of BGB is 3.32%. Assuming that the market's valuation standard for exchange tokens becomes more stringent in 2025, and the ratio rises to 4%:

If on-chain real trading volume is used (excluding zero-fee trades and quantitative arbitrage orders), Bitget's actual effective trading volume may only be 20% of the claimed value. In this case, if the V/MC ratio rises to 5% (a common level in a bear market), the BGB market value will drop to $3.4.

2. Failure of the deflationary mechanism: "paper prosperity" that is not backed by reality

Bitget claims to achieve a 5% annual deflation rate through quarterly token burns, but this mechanism has a double flaw:

- Profit-dependent risk: The burn funds come from 20% of the platform's profits, but Bitget has not disclosed its profit data. If its actual net profit margin is only 15% (Binance is 35%), the annual burn amount = $20 billion (trading volume) × 0.03% (fee rate) × 15% × 20% = $18 million, which can only buy 3.6 million BGB (at $5 per token), accounting for only 0.3% of the circulating supply, far below the 5% deflation target.

- Selling pressure offset: Tokens held by employees and early investors (accounting for 40% of the circulating supply) will be unlocked, and if they reduce their holdings by 2% per year, it will release 24 million tokens, far exceeding the burn volume. The actual circulating supply may not decrease, but increase.

3. Collapse of the ecological narrative: The on-chain dilemma after the BGB and BWB merger

The merger of BGB and BWB was highly anticipated, but on-chain data reveals a cruel reality:

Wallet scenario failure: Although Bitget Wallet claims to have 60 million users, its daily active addresses are only 87,000, with a conversion rate of less than 0.15%. The demand for BGB as a Gas token is almost negligible.

In the event of an extreme situation (such as regulatory crackdown or exchange bank run), the price may further drop below $3.

Conclusion: The domino effect of BGB and the investor's escape window

The "undervaluation" of BGB is essentially a dangerous castle in the air built on high wash trading, weak deflation, and an illusory ecology.

For token holders, the current $5 price level may be the last escape window. When the market realizes that BGB's "deflationary empowerment" is just a mathematical game, the abyss of $3 will no longer be distant.