Author: Wall Street Insight

After the explosive growth of Deepseek, the entire Chinese asset may need to be re-evaluated.

In its latest report on February 5, Deutsche Bank was bullish, stating that 2025 will be the year when China surpasses other countries, and the "valuation discount" on Chinese stocks is expected to disappear, with the A-share/Hong Kong stock bull market continuing and exceeding previous highs. Deutsche Bank said:

2025 is seen as the year when the investment community recognizes China's leadership in global competition. It is becoming increasingly difficult to deny that Chinese companies are providing high value-for-money and quality products in multiple manufacturing and service sectors.

We expect the "valuation discount" on Chinese stocks to disappear, and profitability may exceed expectations due to policy support for consumption and financial liberalization. The bull market in Hong Kong/A-shares is expected to begin in 2024 and surpass previous highs in the medium term.

Specifically, Deutsche Bank stated that China's manufacturing and service industries occupy a global leadership position, and DeepSeek is more like China's "Sputnik" moment:

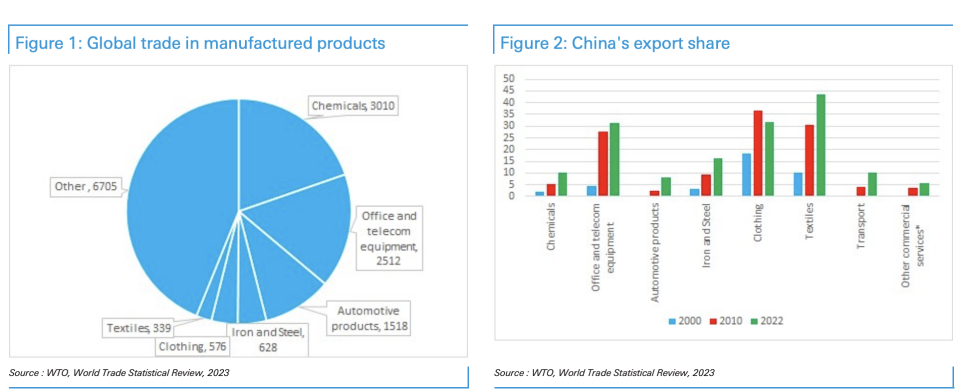

China also occupies a leading position in complex industries such as telecommunications equipment, nuclear power, defense, and high-speed rail, in addition to areas like apparel, textiles, toys, basic electronics, steel, and shipbuilding. In 2025, China launched the world's first sixth-generation fighter jet and its low-cost artificial intelligence system DeepSeek within a week.

Marc Andreessen referred to the launch of DeepSeek as the "Sputnik moment of AI," but this is more like China's Sputnik moment, with Chinese intellectual property being recognized. China is excelling in high-value-added areas and dominating supply chains at an unprecedented pace.

Deutsche Bank believes that China is now in the early 1980s of Japan:

People are starting to realize that China's current position is not 1989 Japan, but rather the early 1980s Japan, when Japan's value chain was rapidly ascending, providing higher-quality products at lower prices, and continuously innovating.

Furthermore, Deutsche Bank is optimistic that the China-US trade issue may bring positive surprises, and trade and markets are not as closely related:

As China's dominant global position continues to consolidate, the valuation discount should ultimately turn into a premium. We believe investors will have to quickly shift towards China in the medium term, and it will be difficult to obtain Chinese stocks without driving up prices.

The Advantages of China's Manufacturing Industry are Increasingly Prominent

In recent years, the advantages of China's manufacturing industry have become increasingly prominent globally.

Deutsche Bank stated:

From its initial rise in the apparel, textile, and toy sectors to its current dominance in areas like basic electronics, steel, and shipbuilding, the development trajectory of China's manufacturing industry is remarkable. Particularly in sectors like home appliances and solar energy, Chinese companies have emerged as strong players.

Notably, China's rise in complex industries such as telecommunications equipment, nuclear power, defense, and high-speed rail demonstrates its strong technological capabilities. By the end of 2024, China's rapid rise in automotive exports attracted global attention, with its high-performance, visually appealing, and competitively priced electric vehicles (EVs) successfully entering the international market. In 2025, China even launched the world's first sixth-generation fighter jet and the low-cost artificial intelligence system DeepSeek within a week, which is seen as an important milestone in the recognition of China's intellectual property.

China's manufacturing strength can be evidenced by the following aspects:

Export scale: China's merchandise exports are twice that of the US, contributing 30% of global manufacturing value-added.

Patent applications: In 2023, China accounted for nearly half of global patent applications. In the electric vehicle sector, China holds about 70% of the patents, and it also has similar advantages in 5G and 6G telecommunications equipment.

Talent pool: Aside from India, China has more STEM (science, technology, engineering, and mathematics) graduates than the rest of the world.

Industrial clusters: China has created local professional clusters similar to Silicon Valley for key industries and collaborates closely with universities in research.

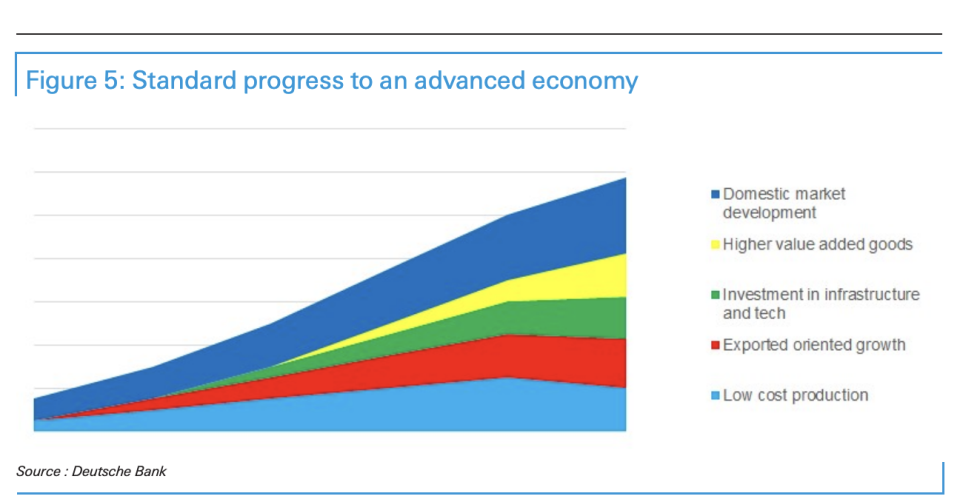

China is More Like Early 1980s Japan

Deutsche Bank believes that China is more like early 1980s Japan:

Japan's growth was achieved through the utilization of abundant cheap labor, capital-intensive use, and productivity improvements. Domestic investment accounted for more than 30% of GDP, thanks to a financial repression policy that maintained low interest rates. Japan acquired new technologies through joint ventures. Savings were around 40% of GDP in the early 1970s and then fell to near 30% in the early 1980s. Japan started setting up factories overseas to avoid trade frictions in the 1970s, which China has only recently begun to do.

Deutsche Bank also stated:

A liberalized financial system is helpful in promoting consumption, as normalizing interest rates will end the transfer of funds from depositors to enterprises. This will reduce over-investment and over-competition, as capital is rationed, which will help improve the returns of state-owned enterprises. We expect that as the returns of state-owned enterprises improve, there will be a demand for easing over-competition to increase stock valuations. We expect this to become a key theme in 2025, and this factor will be a key driver of the bull market.

Furthermore, China's economy and exports are still growing at a relatively fast pace. In 2024, China's exports grew by 7%, with exports to Brazil, the UAE, and Saudi Arabia increasing by 23%, 19%, and 18% respectively, and exports to ASEAN countries along the "Belt and Road" increasing by 13%. China's exports to ASEAN and BRICS countries are now equivalent to the sum of its exports to the US and EU, and its market share in these destinations has grown by two percentage points annually over the past five years.

The drivers of China's economic growth come from several aspects:

Manufacturing advantages: China has world-leading companies in almost all industries and is continuously gaining market share.

The "Belt and Road" initiative: This initiative has opened up regions like Central Asia, West Asia, the Middle East, and North Africa, expanding China's potential markets.

Automation leadership: About 70% of industrial robots are installed in China, driving productivity advantages.

Domestic demand potential: Household savings growth has slowed to twice the nominal GDP growth rate, but savings have increased by $10 trillion since 2020, and these savings are expected to flow into consumption and the stock market in the medium term.

The China-US Trade Issue May Bring Positive Surprises, and Trade and Markets Are Not So Closely Related

According to a previous report by CCTV News, US President Trump signed an executive order on February 1 to impose a 10% tariff on imports from China. However, Deutsche Bank believes the actual situation may be more favorable than expected. The Trump administration seems to value tactical victories more than adhering to ideological positions that are difficult to gain support for.

The launch of DeepSeek has shaken the world's belief that China can be contained. A better approach may be to stimulate business through deregulation, providing cheap energy, and relatively lower barriers to imported intermediate products. A more trade-friendly stance is expected to become part of the evolving "America First" agenda before the midterm elections.

Deutsche Bank's analysis suggests that a rapid China-US trade deal could involve limited tariffs, the removal of some current restrictions, and some large contracts between US and Chinese companies. If this happens, the Chinese stock market is expected to rise.

A decline in exports may actually drive the stock market up for a period. China's dominance in various industries has been achieved through over-investment in many areas. If supply can be constrained, it may benefit stocks and release some capital for domestic consumption.

Overall, Deutsche Bank believes that as China's global dominance continues to consolidate, investors may need to quickly adjust their strategies and increase their allocation to the Chinese market. The Hong Kong/China stock market is expected to continue outperforming global markets in the medium term, continuing the strong performance seen in 2024.

We believe that global investors are often severely underweight China, just as they avoided fossil fuels a few years ago until the market punished those who made non-market decisions. We see a similar pattern in fund holdings of China today. Investors who favor leading companies with moats cannot ignore the fact that it is now Chinese companies that have wide and deep moats, not Western companies.

As the dominant position of Chinese companies continues to consolidate globally, the valuation discount of the China story should ultimately turn into a premium. We believe investors will have to rapidly shift towards China in the medium term, and it will be difficult to gain exposure to Chinese stocks without driving up prices. We have been bullish before, but have been puzzled about what factor will cause the world to wake up and buy, and we believe that China's "Sputnik moment" (or dominance in the electric vehicle space) is that factor.