Title: The People are Tired (of losing)

Author: francesco web3, head of castle labs

Translator: zhouzhou, BlockBeats

Editor's Note: This article delves deeply into the changes in the crypto market, particularly the fatigue felt by retail users. It is not difficult to find that the transition from a venture capital-dominated market to the meme coin craze began in early 2024. Although meme coins once provided a fairer opportunity for retail, they ultimately became too speculative, leading to a deterioration of market conditions. Retail investors are tired of the losses, the market has become fast-paced and highly competitive, emphasizing the importance of finding a new balance point, and calling for more attention to projects with real-world applications and fair issuance mechanisms.

The following is the original content (edited for easier reading):

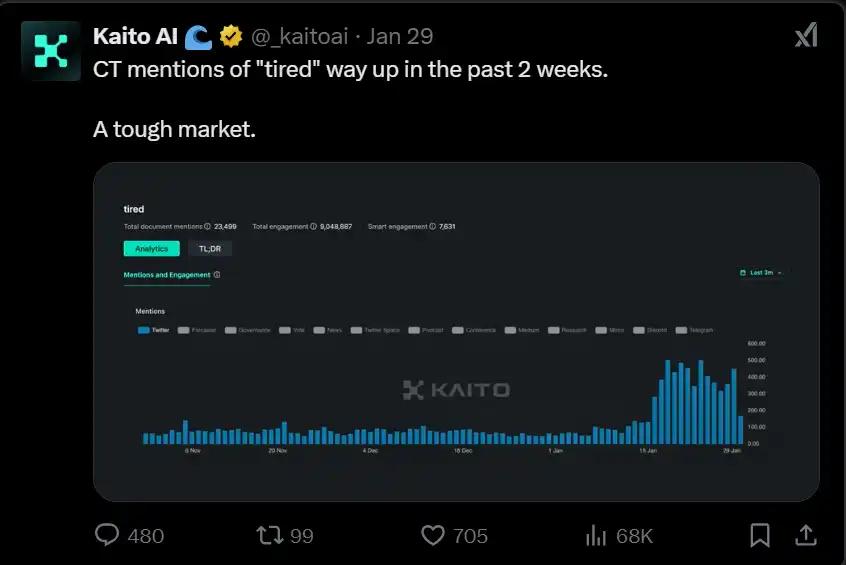

As Kaitoai pointed out, in the last two weeks of January 2025, the word "tired" saw an increase in mentions on Crypto Twitter.

This cycle is different from others, with greater challenges, even surprising traders who have been through two or three cycles. The market is changing: the pace of narrative change is faster, and attention has become the scarcest currency. Last but not least, the increasing regulatory scrutiny and political intervention in the crypto space have brought new variables.

Why are people feeling tired?

Retail investors have missed too many opportunities, and each time the target seems within reach, the market's playbook changes faster than the last. In the 2021 cycle, we saw venture capitalists achieve exponential returns compared to retail investors without private placement opportunities.

This continued until around 2023, when projects like TIA and DYM were launched, marking the end of retail investors' illusion about these venture capital extraction technologies.

What might be the most rational consequence of this? A movement seeking to change the power dynamics.

The long-standing "Meme Coin" narrative has gained more attention as venture capitalists no longer have private stakes to sell to the ignorant market buyers. This was beneficial for retail investors, who managed to find a level playing field. Until the narrative was overhyped and saturated, and the users' attention span further shortened.

Stage 1 (Early 2024) - From VC Coins to Meme Coins

It feels like a long time ago, before the AI hype and meme coin craze, when the mainstream play for retail investors was airdrops. This was initiated by Arbitrum and other Layer 2 airdrops. Retail users saw the possibility of airdrops by trying out new protocols and chains, and airdrops became a business, with airdrop-as-a-service companies emerging.

However, the dream turned into a nightmare when these tokens started releasing and disclosing their token economics, leaving users very disappointed: all the effort, for almost nothing in the end? One of the most controversial releases was Scroll, a ZK-EVM L2.

After over a year of ecosystem promotion, the Scroll airdrop was a huge letdown, with the questionable allocation of 5.5% of the SCR supply to Binance instead of the community.

Additionally, most of these tokens had very low circulating supplies (circulating supply/total supply), and a large portion of the shares were allocated to VCs. Another topic of discussion was TIA and DYM, where the narrative on Crypto Twitter was once about staking them in exchange for the expectation of future ecosystem project airdrops.

You guessed it: those airdrops never happened, and the token price trends have only been downward (the chart below is for DYM).

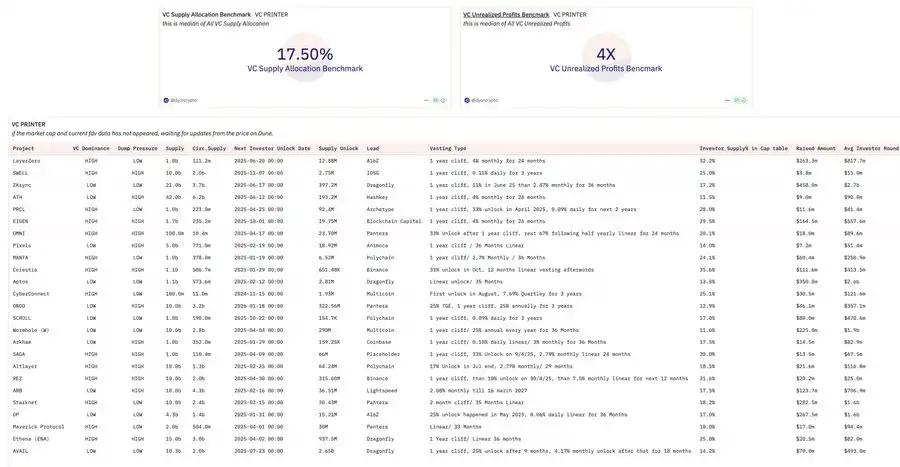

This is an overview of the different rounds and investor unlocks for TIA:

In the first unlock, over 97.5% of the TIA circulating supply was unlocked, worth over $1.88, and the daily TIA unlock volume reached $10 million.

Ultimately, retail investors became tired of these types of tokens, meaning most tokens only went down in price from their issuance, eventually even falling below their last fundraising valuation.

This is evident when we look at the dashboard provided:

This dashboard considers the best-performing investment returns for each VC in the data sample.

Venture capital returns in the previous cycle:

Venture capital returns in this cycle:

The end of the venture capital era is so evident that even Hayes accurately pointed it out in his article in December 2024, and at the end of the dark tunnel, retail investors saw a glimmer of hope: meme coins.

Tired of the venture capital-led conspiracies, retail investors finally had the chance to enter the permissionless market that blockchain was supposed to be open to.

Surely this must be the way forward, right?

Stage 2 - The Meme Coin Craze

After the venture capital era ended, users had to find a new play, and they discovered this through muststopmurad and his "meme coin super cycle".

For retail investors, meme coins seemed to be the closest thing to having an equal opportunity in the market - until they weren't.

Prices went up, Trump got elected, we're going to the moon.

But suddenly, the liquidity plug was pulled, and the market's attention shifted elsewhere, and all your meme coins crashed during the market correction.

Meanwhile, all the early insiders who had the opportunity to position themselves also had the chance to dump their bags. Perhaps the situation retail investors ultimately faced was even worse than what they experienced with VC coins.

What's left now? Becoming more inclined to take risks, further shortening the attention span, liquidity further fragmented, while trying to understand the mistakes they've made through even more gambling disguised as "trading".

Pump.Fun is just a symptom of the direction the market is heading.

jediBlocmates highlighted the net negative issues in this ecosystem.

Among the reasons mentioned, the Pump.Fun team has been constantly transferring large amounts of funds out. In the last month alone, they transferred over 880,877 SOL to Kraken, totaling $211,410,480.

The impact of the meme coin and Pump.Fun craze is evident in the market changes they've brought about: the narrative changes rapidly, the environment has become player-versus-player, and people no longer believe in anything.

Stage 3 - Post-Traumatic Market PTSD: People Feel Tired

After being let down by venture capitalists, users now carry the trauma of the Pump.Fun arena, hoping their next 100x gain can make up for their previous losses. The market has now changed forever, and the new plays are a reflection of this change.

The market rotation is becoming more short-lived and rapid, in previous cycles you could hold opening positions while sleeping, hold tokens for weeks, but now it's at most a few days or hours. New projects are draining all liquidity: attention is scarce, everyone is playing the same game.

The influence of politics and regulation is constantly increasing: this was particularly evident in the launch of TRUMP, highlighting how external events could have an unprecedented impact on the market.

Unfortunately, once again, retail investors have lost their way in this game, with many tokens becoming like the capital extraction mechanisms they are already very familiar with. In contrast to this trend, the launch of Hyperliquidx has drawn attention to community-led airdrops and issuances. Over 31% of the airdrop allocation went to the community, and the token price has increased more than 7-fold since launch, proving that fair issuance can be achieved.

However, it must be considered that not every project can replicate this model, as Hyperliquid, for example, has already incurred tens of millions in massive expenses to run for a long time.

Importantly, the launch of Hyperliquid has brought about a paradigm shift in the industry. Along with the release of Kaito, the way projects approach their launch strategies has also changed.

Where does this leave us?

The stages considered highlight two extremes:

1. Venture capitalists have too much power: retail investors cannot participate in private rounds and can only serve as exit liquidity.

2. Unconstrained meme coin acquisition has led to a player-versus-player market, with overall market conditions becoming worse.

Both have the same consequence: retail investor dissatisfaction and a demand for balance and stability.

We leave some possible thoughts to see what the future might look like: a return to utility, less focus on meme coins, and more focus on utility projects.

Less focus on value extraction, more focus on value creation, avoiding zero-sum games. A return to fair issuance, inspired by Hyperliquid.

A completely new shift in protocol marketing and token release methods, utilizing tools like Kaito for marketing, growth activities, and emphasizing the influence of social graphs and communities.

While we all know that price is the best marketing tool and has always been an important factor in attracting talent and liquidity, it would be a shame to continue focusing on value extraction if a supportive regulatory environment is on the horizon.

The growth cycle of emerging markets is often filled with roller-coaster-like ups and downs, but it is crucial to have an ultimate goal and to map out a viable path for the majority. That is, to build something truly valuable.