Introduction

Despite over a decade of education, adoption, growth, and value appreciation around Cryptocurrencies, Cryptocurrencies continue to face pressure from the U.S. government's stance on the industry - a stance that oscillates between opposition, ambiguity, and tentative engagement. This uncertainty often hangs like a cloud over institutional discussions of Cryptocurrencies. However, our core view has remained unchanged - that the U.S. will be "late but unstoppable" in Cryptocurrencies - and that is precisely the situation unfolding today.

As the Cryptocurrency industry has evolved, many of the debates that once dominated investment decision-making have gradually lost their relevance. Therefore, we advise investors to shed preconceptions and approach this new era of Cryptocurrencies, marked by regulatory clarity and industry adoption, with a fresh perspective.

Looking ahead, distinguishing the most important industry developments from the distractions is crucial, and we must adjust our investment strategies and position sizes accordingly. The legislative process, adoption curves, and emerging technologies will be key drivers shaping the future of the Cryptocurrency industry.

Below, we outline the focus areas our investment team has identified in navigating this rapidly changing landscape.

Accessibility: Expanding Investment Opportunities

As the U.S. adopts a more progressive, definitive, and innovative regulatory posture in digital assets, we expect Traditional Finance (TradFi) entry to help bring liquidity, unlock new capital pools, standardize and institutionalize digital asset investing, and instill confidence in traditional investors to gain exposure to Cryptocurrencies through the familiar, highly regulated brokerage channels. Specifically, we anticipate significant growth in investment vehicles as a wave of ETF products launches, more companies go public via IPOs, and stocks evolve into tokenized securities. This expansion will provide investors with a broader selection, offering greater flexibility to adjust exposures and construct diversified portfolios to suit their needs.

Bitcoin

Bitcoin continues to be institutionalized, with its buyer base expected to further expand into institutional wealth, corporate treasuries, and sovereign wealth funds. Institutions are increasingly viewing Bitcoin as a viable store of value and inflation hedge, while corporate treasuries see it as a strategic asset for diversification and balance sheet enhancement. Driven by monetary stability and geopolitical considerations, sovereign buyers are also beginning to explore Bitcoin as part of national reserves. On the fourth day of his presidency, former President Trump ordered the establishment of a new Presidential Working Group (PWG) to assess the feasibility of creating a national digital asset reserve, having previously promised to create a "strategic national Bitcoin reserve" in Nashville last July.

In December 2024, asset manager BlackRock formally recommended a 1-2% Bitcoin allocation in investment portfolios. Just last week, at the World Economic Forum in Davos, BlackRock CEO Larry Fink revealed that sovereign wealth funds had sought his advice on Bitcoin allocations. These developments may open the floodgates for institutional allocations and drive significant capital inflows into Bitcoin investment products, particularly Bitcoin spot ETFs, as Bitcoin further embeds itself within traditional investment frameworks.

ETFs

Prior to the approval of Bitcoin and Ethereum spot ETFs, investors typically gained Cryptocurrency exposure through hedge funds and trusts. However, these investment vehicles often came with lock-up periods, higher management fees, and higher entry barriers. With the U.S. Securities and Exchange Commission (SEC) approving Bitcoin and Ethereum ETFs, more Cryptocurrency ETFs will enter the market, including single-asset ETFs for assets like Solana (SOL) and XRP, as well as leveraged ETFs, inverse ETFs, and basket ETFs.

However, compared to the success of Bitcoin spot ETFs, the adoption and demand for these new funds may be relatively cautious, as the launch of Bitcoin and Ethereum spot ETFs was a milestone built on years of anticipation. Riskier assets may face lower adoption, while more complex and potentially higher-risk strategies, such as leveraged ETFs, may face longer approval processes. Nevertheless, we expect significant capital inflows into Cryptocurrency products as they become integrated into investment portfolios. This capital influx is expected to help reduce overall Cryptocurrency volatility and alleviate investor concerns about the asset class.

Corporate Financing Instruments

Following MicroStrategy's successful implementation of a Bitcoin treasury strategy, an increasing number of publicly traded companies are tapping capital markets to enter the Cryptocurrency space. Convertible bonds, hybrid securities, preferred equity, and investment-grade or high-yield debt instruments allow companies to raise capital from a diverse pool of investors with varying risk appetites. Convertible bonds and hybrid securities offer investors flexibility and upside potential, while also providing companies with low-cost financing. Investment-grade and high-yield debt expand the channels for institutional capital to access strategic Cryptocurrency investments. These instruments, in turn, provide investors with a broader selection and help them gain exposure to Cryptocurrencies.

IPOs and M&A Activity

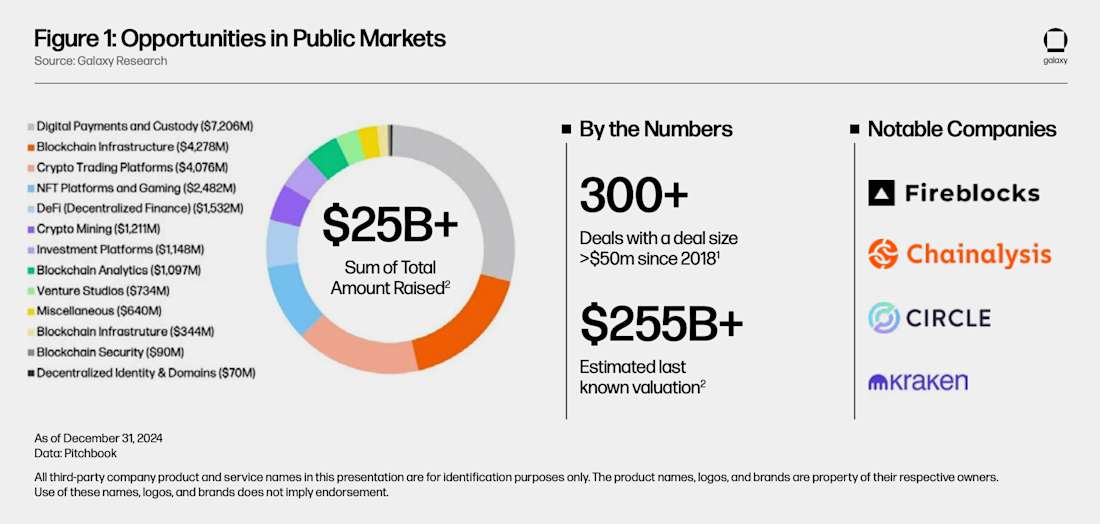

In the venture capital realm, the IPO market will open more meaningfully to domestic Cryptocurrency companies, ultimately paving the way for venture investors to realize returns through exits. Currently, the only venture-backed Cryptocurrency startup (aside from a few special purpose acquisition companies, SPACs) that has gone public is Coinbase, with the majority of other publicly traded Cryptocurrency securities being related to Bitcoin miners. According to our estimates, over 12 Cryptocurrency companies may plan to go public in the U.S. by 2025, spanning trading platforms, blockchain analytics, and custody solutions, among other areas.

The IPO market opportunity is substantial. From 2018 to 2024, over 300 venture deals with individual transaction sizes exceeding $50 million were successfully completed, raising a total of $25 billion - creating a large and diverse pool of companies that can provide public market investment opportunities. The anticipated IPO wave is expected to provide investors and Cryptocurrency funds with more choices, helping them gain exposure to the Cryptocurrency space. Hedge funds and liquid Cryptocurrency strategies may have an advantage over passive funds in capitalizing on these opportunities.

Figure 1 - Public Market Opportunities

Tokenized Securities

Based on the U.S. Securities and Exchange Commission (SEC)'s stance on the Howey test and token disclosures, a new wave of token types may emerge, or existing tokens may add more equity-like features to enhance their value proposition. We anticipate that under the guidance and regulation of a more forward-looking SEC, the tokenization of existing securities (such as U.S. equities) may start to become feasible within regulatory sandboxes and approved proof-of-concepts. An expanded and refined asset ecosystem will help the development of liquid Cryptocurrency hedge fund strategies, driving the maturation and expansion of the investable universe. Improved U.S. token disclosure and issuance capabilities may ultimately challenge or even reverse the current Simple Agreement for Future Tokens (SAFT) model, which favors venture capital (VC) over liquid Cryptocurrency strategies by skewing towards low liquidity and higher fully diluted valuations (FDV).

Structure: Establishing a Robust Institutional Framework

Following the November 2024 presidential election, President Trump began assembling his cabinet to support the development of the cryptocurrency industry. Since President Trump took office, the new administration and Congress have released a series of positive news in the cryptocurrency space. Key developments include President Trump signing an Executive Order (EO) to define the federal government's stance on digital assets, the U.S. Securities and Exchange Commission (SEC) rescinding SAB121 to allow banks to custody crypto assets, and the creation of a new SEC crypto task force "Crypto 2.0". These developments indicate that President Trump intends to mobilize the power of the U.S. government to support the leadership of digital assets and lay the foundation for establishing a robust institutional framework that can facilitate institutional participation. We expect these regulatory changes and national priorities to impact various aspects of financial services, including banking, asset management, sales and trading, and corporate operations.

Stablecoins, Modern Payments, and Dollar Dominance

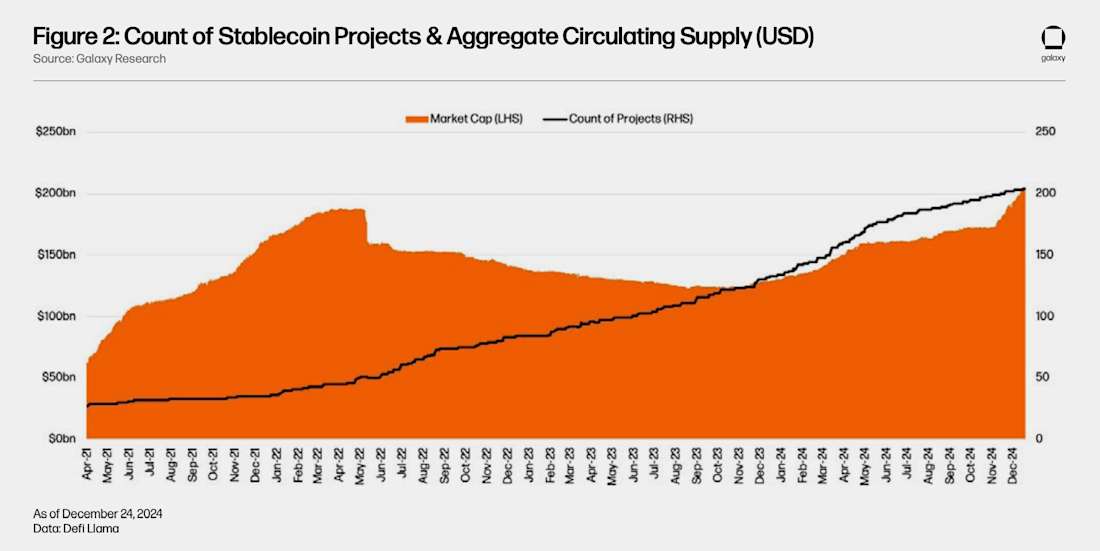

On January 23, 2025, President Trump signed an Executive Order prohibiting the creation of a U.S. Central Bank Digital Currency (CBDC). This move prioritizes privately-led stablecoin projects, which have been viewed as a top priority by the U.S. Congress. In fact, House Financial Services Committee Chairman French Hill (R-AR) has stated that he plans to push for new stablecoin legislation within the first 100 days of the 199th Congress. Stablecoin growth has been rapid, with currently 202 projects, many of which are closely tied to traditional finance (TradFi). This growth is driven by two main factors: the demand for more efficient payment systems and the strategic need to strengthen the global dominance of the U.S. dollar.

Stablecoins have inherent advantages over traditional payment methods, which are often fragmented, analog, and reliant on intermediaries, resulting in higher costs, lower efficiency, and slower speeds, especially in cross-border transactions. In contrast, stablecoin transactions offer lower costs, faster speeds, global reach, and easier integration. These features give them the potential to disrupt the traditional financial system. In fact, this disruption is already evident in their growing transaction volumes, which have increased by approximately 1.6 times year-over-year. According to Visa data, stablecoin-initiated transactions for consumers and businesses are expected to reach around $5.6 trillion in 2024, which is about 3.5 times the total PayPal payment volume in 2023.

In addition to their utility in payments, macroeconomic conditions also support the continued adoption of the digital U.S. dollar. To enhance sovereign debt ownership, coupled with the President's commitment to protecting and expanding the global reserve status of the U.S. dollar, this provides a powerful catalyst for stablecoin growth. For example, asset managers like VanEck and BlackRock are actively partnering with stablecoin projects as part of a broader tokenization strategy to support this goal. As regulatory clarity emerges - and potentially with bipartisan-supported stablecoin legislation in 2025 - we expect major institutions to issue their own stablecoins. These institutionally-backed stablecoins may eventually surpass existing market participants, such as Tether's USDT and Circle's USDC, in the long run.

Figure 2 - Number of Stablecoin Projects and Total Circulating Supply (USD)

Traditional Banks Becoming Self-Custodial New Banks

With the potential for a sweeping reform of the cryptocurrency regulatory landscape, including regulatory changes and new enabling legislation that will allow highly regulated institutions to handle digital assets and interact with blockchains, we expect traditional banks to start offering crypto asset custody and trading services, initiating a process that may gradually transform them into self-custodial new banks. In fact, traditional brokerages like Charles Schwab and Morgan Stanley's E*Trade have already expressed interest in providing direct crypto investment options since the November election.

As a next step, we anticipate that the world's top custodian banks will ultimately custody digital assets. This will mark the beginning of the maturation and institutionalization of the Bitcoin and digital asset markets. For example, once banks can custody Bitcoin and Ethereum, they are more likely to receive approval from the U.S. Securities and Exchange Commission (SEC) to allow physical creation and redemption of spot ETFs. Banks may also start providing lending and financing services for digital assets, such as margin trading collateralized by Bitcoin, or create innovative structured products to provide customized exposures to underlying digital assets. As bank infrastructure begins to support cryptocurrencies, we can expect digital asset investment products to become more diverse in type, better designed, lower in cost, and more naturally integrated into investment portfolios.

Enterprises Launching Their Own Blockchain Networks

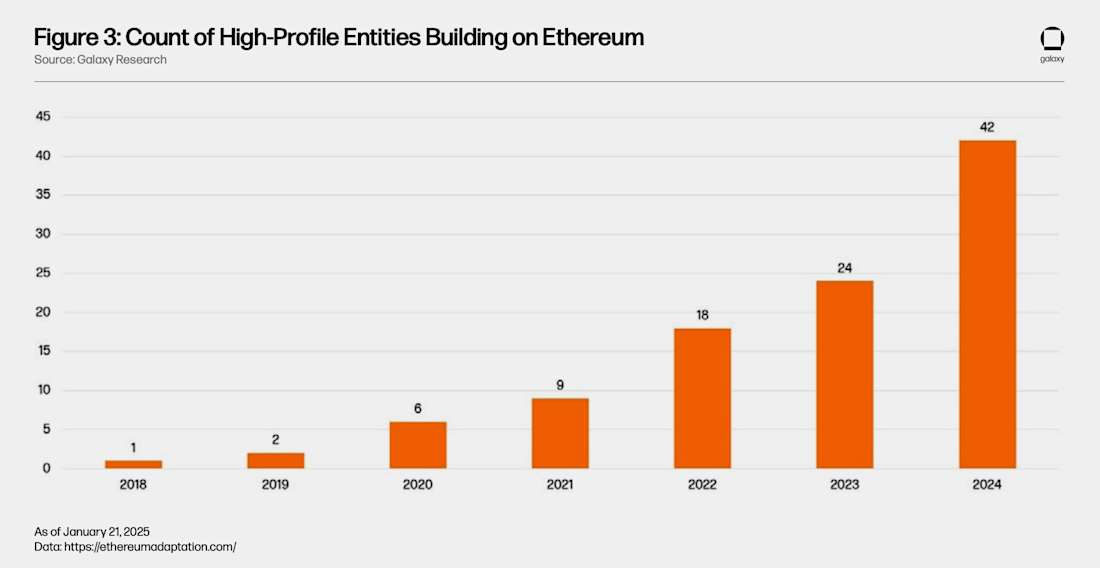

Since JPMorgan Chase created the blockchain-based platform Onyx (now called Kinexys) in 2020, many enterprises have launched pilot projects to explore blockchain technology. These projects often leverage Ethereum for tokenizing real-world assets (RWAs), issuing stablecoins, and minting non-fungible tokens (NFTs). According to our estimates, over 50 companies, including 13 financial institutions, are actively building projects on Ethereum-based platforms.

Recently, we have seen more enterprises launching their own Layer 2 (L2) scaling blockchain solutions on top of major Layer 1 (L1) blockchains. Notable examples include Coinbase's Base network, Kraken's Ink, Deutsche Bank's L2 blockchain, and Sony's Soneium. These companies are using L2 designs to build systems tailored to end-user needs while maintaining data transparency, auditability, and efficiency. These systems are being applied to construct Know-Your-Customer (KYC) and Anti-Money Laundering (AML) ledgers, and to create ecosystems for gaming, finance, and entertainment applications.

Overall, we are witnessing companies actively testing the capabilities of blockchain smart contracts to enhance existing traditional finance (TradFi) infrastructure. We expect more enterprises to start exploring the potential of blockchains, developing controlled, open, or closed systems that fit their operational requirements.

Figure 3 - Number of High-Profile Entities Building on Ethereum

Sharing Fundamental Values with Decentralized Finance (DeFi) Users

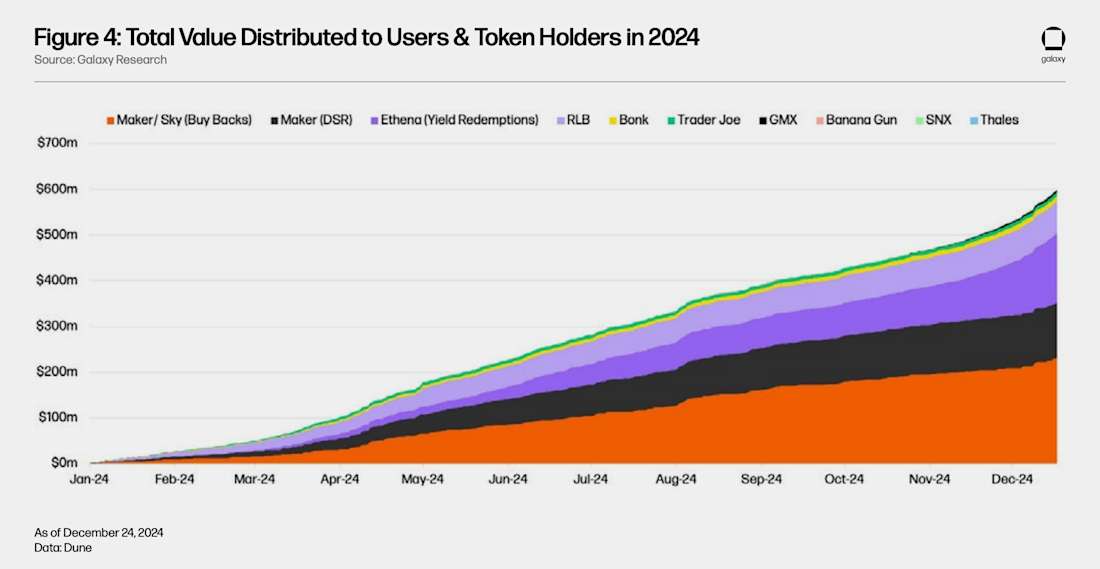

With the U.S. Securities and Exchange Commission (SEC) relaxing the application of the Howey test to digital assets, potentially expanding the definition of crypto assets as securities, allowing brokers and traders to transact in these assets, the scope of value sharing within crypto protocols is expected to expand. The third-largest stablecoin protocol Ethena and the long-standing lending protocol Aave have already initiated discussions or passed proposals to implement their "fee switch" mechanism, which can distribute value to token holders. Other protocols, including Uniswap and Lido, which previously rejected such mechanisms, may reconsider their stance due to regulatory clarity and market competitive pressures. As more value accumulates within on-chain protocols, buybacks and direct revenue-sharing mechanisms are expected to occur more frequently and at higher rates.

Historically, the value generated by protocols has primarily been distributed among liquidity providers (LPs) and the protocol or decentralized autonomous organization (DAO) treasury, with token holders unable to benefit from the rewards generated by the core application activities. Earnings paid to token holders are often mistaken for value distribution, when in reality they are usually achieved through the release of more token supply into circulation, leading to inflation (such as through staking or airdrops). The introduction of buyback mechanisms and revenue-sharing structures is expected to address this imbalance. As a result, token prices based on network fundamentals are expected to receive positive support, particularly for assets related to lending applications, crypto-backed stablecoins, liquid staking, base yield platforms, perpetual decentralized exchanges, and yield farming protocols.

The evolution of the buyback mechanism has made cryptocurrency tokens more akin to stock securities, providing legitimate value to holders. Previously, due to the design of these protocols, token prices lacked a sustained value accumulation driver. Through these new mechanisms, token prices can begin to reflect their underlying utility and revenue generation, providing a more attractive investment case for token holders.

Figure 4 - Total value distributed to users and token holders in 2024

Growth: The Emerging Frontier of Digital Infrastructure and Interaction

As the cryptocurrency industry continues to evolve, new innovations are emerging at the intersection of crypto and artificial intelligence (AI). The rapid development of AI technology makes its integration with crypto both inevitable and far-reaching, as they both share fundamental principles of data processing and efficiency. This synergy is creating opportunities for crypto infrastructure providers to accelerate the growth of the AI industry and open new frontiers in areas such as gaming, digital identity, automated trading, and quantum computing. For investors, these developments present attractive opportunities.

Bitcoin Mining Transitioning to AI Computing

With the growing demand for AI-driven computing, Bitcoin miners are expected to retrofit, build, or co-locate with existing mining facilities to leverage high-performance computing (HPC) infrastructure. This integration will allow miners to remain competitive and explore dual-use cases to maximize efficiency and profitability.

Both Bitcoin mining and high-performance computing require extensive energy infrastructure and world-class data center architecture, a natural fit that enables Bitcoin miners to meet the demands of hyperscale computing. By leveraging existing infrastructure and developing refined energy strategies for both mining and AI computing, Bitcoin miners can open new revenue streams and create additional value. However, only miners with the right infrastructure and adaptability will be able to seize these opportunities. We believe miners with large-scale land, water for cooling, dark fiber, reliable power, technical labor, energy approvals, and critical long-term infrastructure are in a favorable position to increase asset value, while other miners may become less competitive over time and undergo consolidation.

Concurrently, spatial computing technologies aim to recreate real-world user experiences through digital means, providing additional synergies for Bitcoin mining and AI computing. Spatial computing is driving advancements in processing technologies, data privacy, and streaming capabilities. As these developments progress, particularly with the increasing importance of gaming technologies like graphics processing units (GPUs) in these industries, the enhancements to HPC and Bitcoin mining operations will become more pronounced.

As these trends unfold, large-scale Bitcoin miners present an attractive investment opportunity, while spatial computing may emerge as an undervalued domain. Although Bitcoin miners currently hold a significant share in investment portfolios, their share may decline over time as the industry consolidates and more companies go public.

AI-Driven Web3 Gaming Experiences

Since the inception of Web3 in 2014, Web3 gaming has primarily focused on in-game economies, utilizing NFTs and play-to-earn mechanics to incentivize community participation. However, after the hype around projects like Axie Infinity and STEPN, the industry has experienced a decline in momentum. To regain player interest, games like Gunzilla Games' "Off the Grid" are shifting their focus back to player experience. Developers are increasingly integrating Web2 technologies to create smoother gaming experiences, significantly improving overall quality and enhancing the appeal of Web3 games.

Concurrently, advancements in AI technology are opening new possibilities for enhancing the playability of Web3 games. AI-driven tools are shortening production cycles, allowing developers to prioritize innovation and deliver higher-quality games. For example, AI-driven non-player characters (NPCs) are continuously evolving, providing dynamic and personalized gaming experiences that can adapt to player behavior.

With these developments, high-quality and well-designed Web3 games are poised to drive industry growth through widespread adoption by major publishers and developers. For instance, Ubisoft's "Champions Tactics: Grimoria Chronicles" allows players to assemble virtual warriors through minted NFTs to compete against other players.

The convergence of AI and blockchain technology presents an opportunity for accelerated adoption of Web3 games, with enhancing the player experience as the core driver of this process. We expect that by 2025, Web3 games will make significant strides in player experience, gradually blurring the lines between Web3 and Web2 games, while also integrating gaming communities with blockchain technology.

Conclusion

We believe that the cryptocurrency industry will achieve meaningful growth in 2025 through a transition from speculative cycles to practical applications, redefining the digital economy. Driven by favorable top-down regulatory changes, new government support, and through industry maturity and increased accessibility, the market's openness to the cryptocurrency industry will create new ideas and opportunities for industry growth and widespread adoption.

While some aspects of this evolution will lead us towards new economic concepts and paradigms, many developments will appear similar to the status quo. For example, the integration of crypto and traditional markets is accelerating through the addition of crypto-native functionalities (such as the in-kind creation and redemption mechanisms in ETF products and staking activities) and traditional financial activities (such as IPO issuances and M&A activities).

However, 2025 may also mark the beginning of a multi-year cycle of widespread adoption and integration of new blockchain technology applications that will shape our world and markets. We expect that over time, many applications will gradually emerge - the synergies between crypto and adjacent technologies like artificial intelligence, gaming, and spatial computing are opening new possibilities. Bitcoin miners are adjusting their operations to meet the growing demand for high-performance computing from AI, while Web3 games are transforming player experiences through AI-driven advancements. These intersections represent the next wave of innovation, pushing the boundaries of technology and finance.

We believe this year will redefine how value is created, captured, and utilized in the cryptocurrency industry. At Galaxy, we are committed to building, investing in, and interpreting these industry-transformative transitions.